Use of Islamic finance in Spain hindered by banking laws

Despite calls from Spanish businesses for the government to facilitate greater access to the $2 trillion Islamic finance market, the country’s banking and tax legislation is blocking the way

Due to the underlying structural problems that continue to plague the Spanish economy, parts of the country’s business sector have been calling for modifications to national laws that would encourage the use of Islamic finance, but leading lawyers say Spain’s banking and tax regulations are not suited to this form of finance.

Though Spanish government statistics showed that the number of registered employees in Spain rose by more than 540,000 in 2016, critics argue that the country’s economic prospects, while looking fairly positive in the short term, are quite bleak when a longer term perspective is taken. They say that there are structural problems in the labour market, specifically too many temporary and short-term contracts, as well as low salaries and low productivity.

Ethical lending

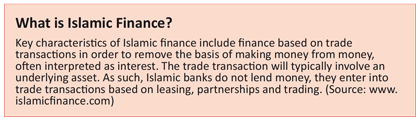

Given these conditions, businesses in Spain have called on the government to help facilitate the greater use of Islamic finance. Among the promoters of this type of finance is the Saudi-Spanish Centre for Islamic Economics and Finance (SCIEF), which works in partnership with the IE Business School in Madrid. Among the key characteristics of Islamic finance are the prohibition of the accruement of interest, the requirement that lending is ethical, as well as the prohibition of speculative lending, which is viewed as gambling. For example, with regard to the condition related to ethical financing, SCIEF highlights that an institution proving Islamic finance would not be willing to finance a casino or a company producing pornographic material.

It is estimated that the global market for Islamic finance is now worth $2 trillion and the UK, in particular, has spotted the potential for utilising this type of finance. There are believed to be more than 20 international banks with Islamic finance operations, while more than 20 law firms with offices in the UK currently offer legal services related to Islamic finance.

Untapped market

However, so far Spain has largely failed to tap into this potentially lucrative market, despite high demand for such finance from the country’s business sector. Guillermo Canalejo, partner at Uría Menéndez in Madrid, says the use of Islamic finance in Spain has been very limited. He adds: “With the exception of the UK, the presence of Islamic investment in Europe has been of little significance, but countries such as France, the Netherlands and Luxembourg have taken the necessary steps to facilitate the arrival of such funds.”

Canalejo says that Spain’s banking, regulatory and tax regulations are not suited to contracts and practices governed by the precepts of Sharia law. He adds the Islamic alternatives to traditional mortgage agreements, for example, would require modifications to Spanish laws, and there are regulatory obstacles and tax penalisations that hinder the use of such alternative financing. Canalejo says that a key advantage of Islamic finance is its abundance, while the SCIEF says that Islamic finance offers numerous advantages including ensuring greater social justice, for example.

“There is no doubt that Spain, as with other countries in Europe, is a particularly attractive market for foreign investment, including Islamic investment,” says Canalejo. He adds: “Spain’s business sector and institutions have been promoting the introduction of the necessary measures to make Spain a more ‘friendly’ country for such alternative financing.” In this respect, Canalejo highlights the “extraordinary lobbying” carried out by IE Business School and the SCIEF.

But despite the positive steps taken, more needs to be done to foster an environment in Spain that is receptive to Islamic finance, according to Canalejo. “Greater support from government institutions is vital, without this the project to make Spain an attractive market to such investment funds, or at least a market that does not penalise Islamic finance, will not be realised.”