Reshaping your firm

The financial crisis dealt a severe blow to many firms but also presented an opportunity for strategic renewal. How many law firm leaders have taken this opportunity? Exclusive research commissioned by Iberian Lawyer explores which firms have adapted best

Times have been tough since the start of the financial crisis. But as the saying goes, when the going gets tough, the tough get going. How many times, since 2007, have lawyers discussed seeking new opportunities during difficult times? “The crisis is too good an opportunity to miss,” has been the mantra of more than one law firm leader.

Exclusive research commissioned by Iberian Lawyer now helps show which of Spain´s leading firms have had a “good” crisis. Which firms, if any, have reshaped and refocused their practice and are now emerging in a stronger position than their competitors?

The annual data prepared by Expansión, the Spanish business newspaper, provides an overview of the changing shape and size of the top firms in Spain. This year, for the first time, Iberian Lawyer asked London-based consultants Redstone – the world´s largest consultancy advising law firms – to analyse the Expansíon data: what has the crisis meant for law firms in Spain and what should we expect next? “By comparing the Expansión data for 2008 and 2013, we can start to analyse the changes that the Spanish legal market has seen throughout the crisis years,” says Redstone managing partner Steve Blundell. “We can see that the worst is now behind us and get an idea of the changes which we should be expecting next.”

More than a statistical analysis, the new methodology aims to understand how the crisis impacted on different types of law firms and see which firms have outperformed their competitors – numbers are averaged. Redstone´s methodology applies Expansión´s data to two issues: the nature and type of work undertaken by different groups of firms and their financial success. The former is illustrated by changes in “Income per Lawyer” – the firm´s turnover divided by total number of fee earners. Income generated by each individual lawyer in a firm indicates hourly fees, and therefore, type of work being undertaken – be that higher or lower value. Knowing if this translates into financial success is more difficult – as costs are not included in the Expansión data, it is not possible to calculate profitability. In this case, Redstone divided turnover by number of equity partners indicating Income per Equity Partner. This does not reveal Profit per Equity Partner, but as law firm costs are broadly similar, and grow equally with size, the broad market changes become evident.

The good news is that the legal market is growing – turnover increased an average of 3.87 per cent among the top 20 firms in 2013, nearly double the 2012 figure. To some surprise, the economic climate has not deterred new arrivals – White & Case and Clyde & Co last year being the latest in a list of market entrants. Meanwhile, the legal arms of the international auditors are continuing their growth unabated. In total, of the Top 10 legal providers, only four are Spanish.

The pre-crisis picture

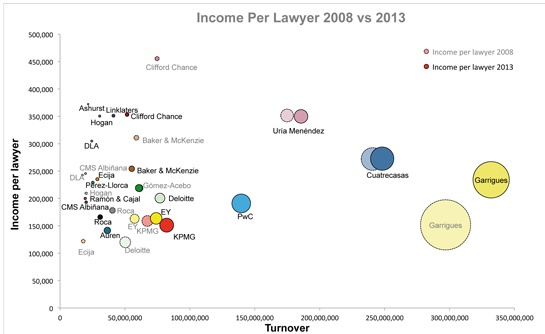

The pre-crisis data illustrates the different approaches being adopted by different parts of the market. As the largest law firm in continental Europe, with 2008 turnover at almost €300m, size was the traditional driving force at Garrigues – in the charts the number of professionals in the firm is reflected in the size of their bubble – with the smaller Cuatrecasas, Gonçalves Pereira and Uría Menéndez positioned to the left.

But when reviewed in the context of Income Per Lawyer, different strategies begin to emerge. With their emphasis on only ´higher value´ work-types, the UK firms have a ´smaller and better´ approach. In 2008, Clifford Chance was the highest in the Income per Lawyer axis at €455,000 – higher than the much larger Garrigues at €152,000. As Clifford Chance´s fellow Magic Circle firms – Allen Overy, Freshfields and Linklaters – do not participate in the Expansión survey, the assumption is that their Income Per Lawyer is similar.

Pre-crisis, the bottom left quadrant of the charts was the most crowded – the majority of the firms share a very similar market position, that is, neither the biggest nor commanding the highest Income per Lawyer in the market.

Prices fall

The 2013 data, when compared to 2008, provides the clearest picture of the storm damage. Aside from the huge fall in transactional work, the early crisis period saw client demand for high value expertise rising. “From the data, however, it is clear that they did not want to pay the same rates as before,” Moray McLaren, Redstone partner, says. In general, faced with the challenges of falling prices and decreasing transactional work, firms have been largely forced to reduce lawyer numbers to maintain profitability.

A snapshot of five-year revenues and lawyer numbers shows decreasing turnover, but firms were reducing their number of lawyers to maintain their Income per Lawyer. By cutting lawyer numbers and gaining efficiencies, firms were able to combat declining revenue and return – on average – slight increases in Income per lawyer. In total, lawyer numbers fell 19 per cent.

The drop in Income per Lawyer at Clifford Chance from €455,000 to €353,000 shows the market switching, and it would be interesting to know how that compares with its other offices around the world. And while Clifford Chance had been alone at the top of the Income per lawyer scale in 2008, by 2013 it had been joined by Ashurst, Hogan Lovells and Linklaters. Competition is getting tougher – a convergence of the international firms, focusing on higher value services rather than size, is emerging in the top left corner of the “Income Per Lawyer 2008 vs 2013” chart.

The domestic firms performed better. With the downsizing and reorganisation at Garrigues, the Income per Lawyer actually rose over the five years from €152,000 to €234,000. Also against the trend, Cuatrecasas and Uría Menéndez maintained their Income per Lawyer.

Presumably, this is due to managing costs – the lawyer numbers fell at Garrigues by 27 per cent – and reshaping their practices to the changing market needs. It could be that the wider practice spread made them less vulnerable to decreasing transactional work, while with a high domestic brand positioning, they were better suited to, and were first choice to advise major Spanish businesses in difficulty.

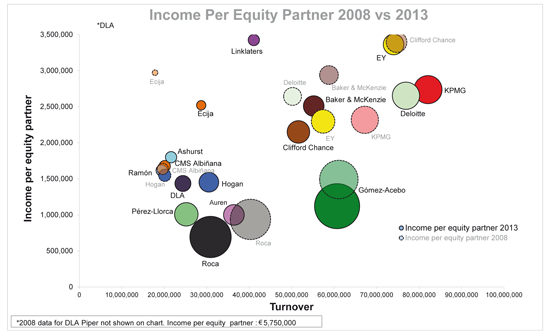

Income per Equity Partner

When comparing 2008 Income per Equity Lawyer data, differences in approach emerge. With just 92 equity partners in 2008, and an Income per Equity Partner of €3.2m, the outputs of the Garrigues model become clear. This was despite a middling Income per Lawyer figure that year of €152,000. Even when building a wider full service firm, many Spanish firms have kept ownership tight. Last year, with only four equity partners and a turnover of almost €15m, Valencia-based Broseta´s €4.4m per equity partner was higher than London´s Magic Circle.

The crisis brought new approaches. Moving away from restricted ownership, with a large salaried partner group, Garrigues were first to change direction. Widening ownership, it welcomed a large group of salaried partners into equity – in one move creating a grateful new group of owners while rebalancing financial risk. By 2013, Income per Equity Partner had dropped to €1.3m, which may not make headlines but builds a stronger firm. Cuatrecasas followed, moving salaried partners to equity, increasing equity ranks from 127 to 202 over this period and reducing Income per Equity partner from €1.89m to €981,188. Neatly, the selection process also provided an opportunity to remove those unsuitable for promotion.

According to Expansión, after a period of decline total lawyer numbers at the Top 56 firms by revenue are growing – a 0.71 per cent increase in 2012 then 1.8 per cent in 2013. A small but highly significant change. Some firms are not at their ideal size. While Garrigues continues to reduce capacity, with a 7.9 per cent reduction in lawyers in the last year, Pérez-Llorca increased lawyer numbers by 8.6 per cent.

Game changing

As the charts show, the legal arms of the accountants deserve the most credit. Income per Equity Partner at Ernst & Young (now EY) and KPMG has risen by 47 and 18 percent respectively. At €4.4m, Income per Equity Partner at Landwell PwC is second only to Clifford Chance. Since last year, from the Top 10 firms only Cuatrecasas, Deloitte, Garrigues, PwC and Uría Menéndez have raised their Income per Lawyer.

In conclusion, Blundell says Spain has seen massive change in a short time. “The market changes are similar to those in other markets but the rate of change in Spain has been exceptional.” In all jurisdictions, he adds, research shows legal markets polarising – different strategies are becoming clearer – with a clustering of firms in each part of the chart. But not many jurisdictions alter so much over a five-year period, Blundell says.

The UK firms, with their increasing emphasis on specific higher value services, are grouping around Clifford Chance in the top left quadrant. Meanwhile, unlike most European markets, the Spanish market remains led by locals – with Garrigues reporting revenue of €300m and Cuatrecasas and Uría Menéndez posting more than €150m. The crisis has shown their resilience but also ability to take tough decisions and adapt their approach. It is the rise of the Big Four auditors that poses the main questions. As good lawyers have left the major firms, the auditors have enjoyed an opportunity to grow at low cost – without high investment in training and development.

But whose work will they win? It is said that the auditors opportunity is more standardised work but that could be outdated. The rise in Income per Lawyer suggests the Big Four are muscling into the high value legal services arena with notable success.

The full results of the Redstone research are available on request from fiona.mccambridge@redstoneconsultants.com